Depending on your employer’s program policy, benefit accounts can have different rules on whether balances expire if you don’t spend them by a certain date, or whether they roll over until they reach a maximum balance.

Benefits with expiring balances don’t allow roll over or will only allow rollover for a certain period of time. Any leftover balance after the expiration date will be forfeited.

Example 1: Funding Renewal and Expiration Periods Are the Same

You have a benefit that provides you with $30 on the first day of each month. If you've spent $20 so far this month, you'll have a remaining balance of $10. If the benefit has a monthly expiration, any unused balance will not roll over. On the first day of the next month, you'll receive another $30, and the unused $10 from the previous month will be lost, leaving you with a new balance of $30.

Example 2: Funding Renewal and Expiration Periods Are Different

You have a benefit that provides you with $50 on the first day of each month. If you've spent $20 this month, you'll have a remaining balance of $30. If the benefit follows a quarterly expiration policy, any unused funds can roll over to the next month or until the end of the quarter. So, next month, you'll receive another $50 and your remaining $30 balance will roll over, giving you a total of $80.

Benefits with maximum balances do allow unused balances to roll over when you get your next deposit, until you reach a maximum balance set by your employer.

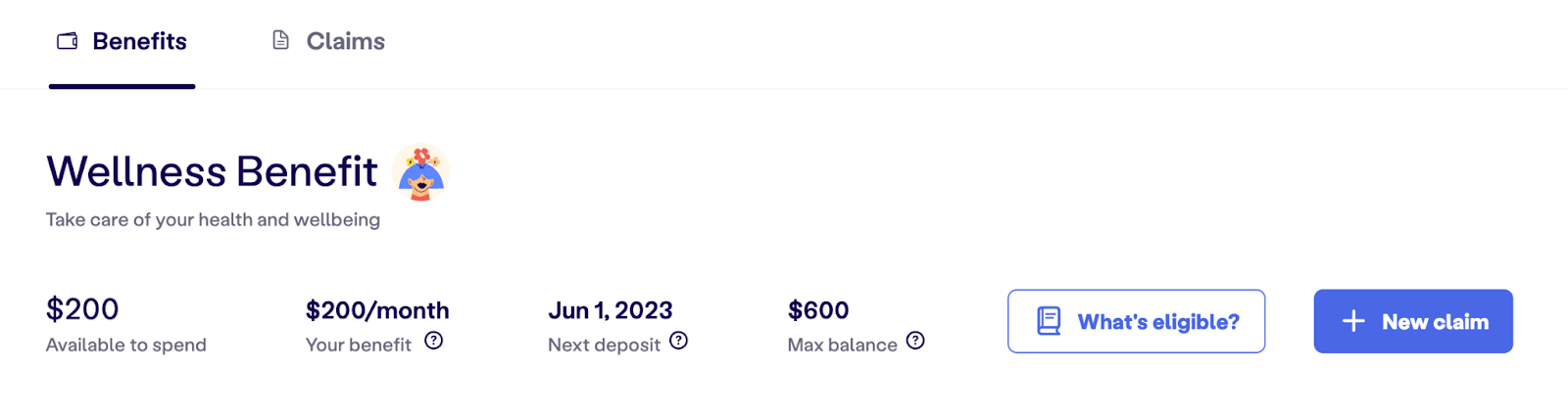

For example, imagine that you have a benefit where you receive $50 on the first day of each month, with a maximum balance of $200. If you don’t spend the full amount by the end of the month, you’ll still get your next $50 deposit on the first day of the next month, and your balance will accumulate until it reaches $200. Then it's capped and you won’t get additional deposits until you spend down the balance.

You’ll still get a partial deposit if you haven’t reached the maximum balance — so if you have $180 remaining at the end of the month, you’ll get a $20 deposit to reach the maximum balance of $200.

You can tell which benefits have a maximum balance at the top of the benefits detail page:

You can check if any of your accounts have expiring or maximum balances in your employer’s program policy.